With yields on global fixed income close to record lows at 0.9%, investors in classic bonds are left vulnerable to a potential rise in rates, with only limited income buffer. Our approach is different and has in the past shown itself to be resilient to rate rises. Given the most recent rise in US rates, we have received several queries from investors, asking us if we believe this is a concern for our strategy and the fund. Our response has been straightforward: “No, on the contrary”. The reason for this is twofold: i) We have positioned the fund to have low sensitivity to rates and ii) Subordinated debt, especially subordinated debt issued by the financial sector, tends to benefit from a rising rate environment.

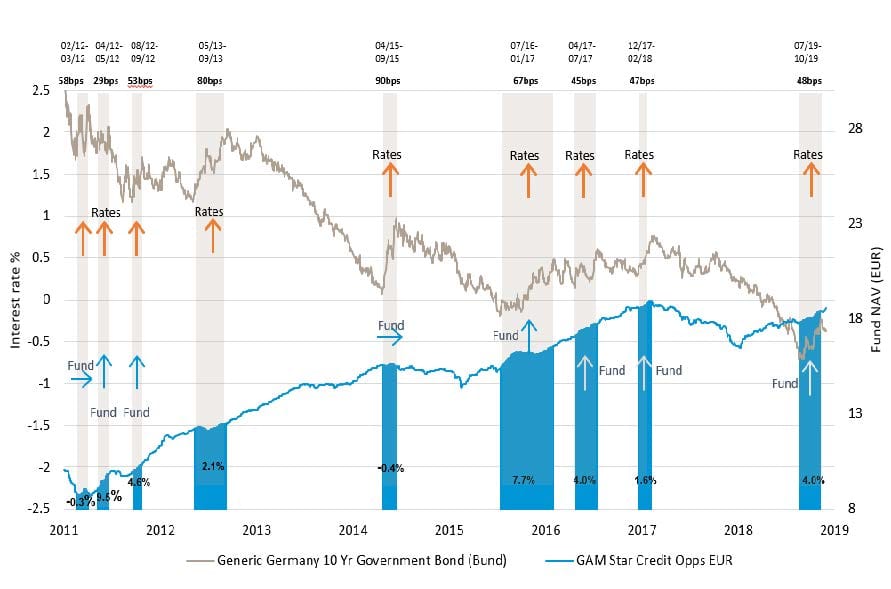

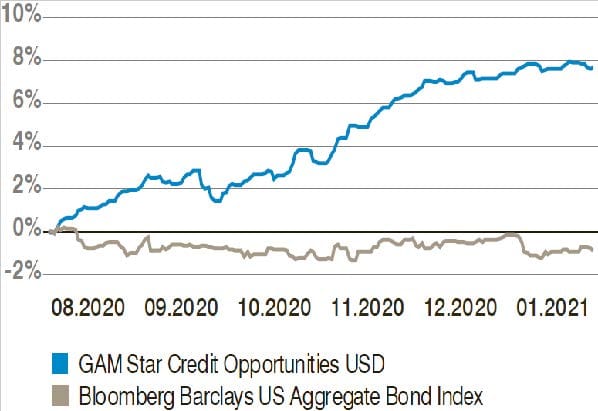

i) The fund is positioned to have low sensitivity to rates: In the US, rates have rebounded since early August, as the 10-year US treasury moved up from 0.5 to 1.1%, weighing on USD-denominated fixed income. While we expect a lower for longer interest rate environment, higher rates remain a threat for many bondholders especially as central banks have de facto forced many fixed income investors into taking more duration risk to compensate for the low / negative interest rate environment. In contrast, the fund is constructed to have limited sensitivity to interest rates, by using a combination of fixed rate, floating rate and fixed-to-floating instruments. Historically the fund has had very low sensitivity to rising rates, mainly generating strong performance during times of higher interest rates, see chart 1. Recently this has remained consistent with our EUR, GBP and USD funds all returning circa 8% since August 2020, while US interest rates have risen by more than 50 bps and US fixed income returned close to -1%, see chart 2.

Chart 1: Performance of EUR fund during periods of rising rates

Source: GAM. Data from December 2011 – December 2019. Past performance is not an indicator of future performance and current or future trends.

This can partly be explained by the fact that although subordinated debt is typically long-dated or perpetual, bonds are often fixed-to-floating, meaning that the coupon is reset periodically, therefore offering limited duration risk on top of high income. Additional Tier 1 Capital Contingent Convertibles (AT1 CoCos), for example, yield slightly above 4%, compared to 0.9% for global bonds, while duration is around half at 3.7 for AT1s compared to 7.4 for global bonds – meaning that AT1 holders have both high income (ie higher ability to absorb price declines) as well as significantly lower sensitivity to rates should rates rise.

ii) Subordinated debt, especially subordinated debt issued by the financial sector, tends to benefit from a rising rate environment:The financial sector directly benefits from higher rates as higher rates lead to higher profitability, stronger earnings and lower cost of equity. This is also supportive in terms of credit fundamentals and normally leads to tighter credit spreads, ie price appreciation.

Chart 2: Performance of USD fund versus Bloomberg Barclays US Aggregate Bond Index

Source: GAM, Bloomberg. Data from August 2020 – January 2021. Past performance is not an indicator of future performance and current or future trends. For illustrative purposes only. USD fund example used in relation to US interest rates.